Debt recovery in Poland requires more than sending reminders. A creditor should first verify the debtor, prepare evidence, attempt pre-court recovery and only then decide whether litigation and enforcement are commercially justified.

For foreign creditors, the key practical issue is simple: a Polish court judgment is useful only if the debtor has assets that can later be enforced against. This is why the process should start with a realistic assessment of the debtor’s financial position.

Creditors doing business in Poland may also benefit from reviewing broader legal and market entry considerations available in the Investor Zone by Dudkowiak & Putyra, especially where unpaid debts arise from commercial cooperation with Polish counterparties.

Debt recovery in Poland – process at a glance

| Stage | What happens | Practical purpose |

| Debtor verification | Checking registers, financial statements and available asset information | Assess whether recovery is realistic |

| Demand for payment | Formal notice sent to the debtor | Create pressure and evidence of amicable attempt |

| Settlement talks | Negotiating instalments, postponement or security | Recover faster or strengthen creditor’s position |

| Court proceedings | Filing a statement of claim with evidence | Obtain judgment or order for payment |

| Bailiff enforcement | Enforcement against bank accounts, assets or receivables | Convert judgment into actual recovery |

| Cross-border enforcement | Recognition or enforcement abroad, if needed | Reach debtor’s assets outside Poland |

This structure helps creditors avoid a common mistake: moving directly to court without checking whether the debtor has any recoverable assets.

Step 1: Verify the debtor before taking action

Before starting debt recovery in Poland, the creditor should check the debtor’s financial situation and assets. In the case of Polish companies, this may include the National Court Register, financial statements, performance reports and information on public-law arrears, bankruptcy or restructuring proceedings.

A company’s failure to file required financial statements may be a red flag. Financial documents may also show whether the debtor owns valuable assets, how high its liabilities are and whether it has generated profits in recent years.

Verification of individual debtors is more limited, as natural persons do not publish financial statements. Still, available registers may show bankruptcy, restructuring or disqualification from running a business.

In practice, debtor research may also include online checks, credit reference agencies, debt registers, detective services or court enquiries concerning bankruptcy, restructuring or enforcement matters.

Step 2: Send a demand for payment

A demand for payment is usually the first formal step in pre-court debt recovery. It shows that the creditor is taking the claim seriously and may encourage the debtor to pay or open negotiations.

The demand also matters if the case later goes to court. It may prove that the creditor attempted to resolve the dispute amicably and may help establish when the claim became due and payable.

A practical demand for payment should include:

- date and place of issue;

- full creditor and debtor details;

- legal basis of the debt, such as invoice, contract or agreement;

- exact claim amount, including interest date;

- payment deadline;

- bank account for payment;

- creditor’s or representative’s signature;

- proof of delivery.

The demand should usually be sent by registered letter with acknowledgment of receipt. An email copy may be useful as supporting evidence, but it should not replace reliable proof of delivery.

Step 3: Consider settlement – but secure it

An out-of-court settlement may save time and costs. Typical settlement terms include payment in instalments, postponement of the payment date or partial waiver of interest.

However, creditors should remember that an ordinary out-of-court settlement is not automatically enforceable by a bailiff. If the debtor defaults, the creditor may still need to start court proceedings.

For this reason, settlement should be secured where possible. Depending on the case, useful tools may include a blank promissory note, third-party suretyship or the debtor’s submission to enforcement in a notarial deed.

A practical settlement checklist should cover:

- exact debt amount;

- payment schedule;

- consequences of default;

- security instrument, if available;

- acknowledgement of debt by the debtor;

- signatures of authorised persons.

The best settlement is not merely a compromise. It should give the creditor a stronger position if the debtor stops paying again.

Step 4: Use additional pre-court pressure where appropriate

If the debtor ignores the demand, the creditor may instruct a debt recovery agency or a law firm. Their role is usually to contact the debtor, send letters and support settlement discussions, but they cannot seize bank accounts or assets.

Another option is selling the overdue debt. This may allow the creditor to recover at least part of the amount without continuing the entire recovery process.

The creditor may also consider reporting the debtor to a public debt register. For non-consumer debtors, the overdue amount must exceed PLN 500 and be overdue for at least 30 days; for consumer debtors, the threshold is PLN 200.

Before reporting a debtor, the creditor must send a notice of default and be able to prove it. This again makes proper documentation of the demand for payment essential.

Step 5: Prepare the court claim

If pre-court recovery fails, the creditor may file a lawsuit in Poland. Before doing so, the creditor should collect evidence, assess costs and prepare a litigation strategy.

A statement of claim should identify the court, the parties, their addresses and attorneys, if any. It should also state precisely what the creditor is claiming, including principal amount, late-payment interest and litigation costs.

In a straightforward payment case, the key evidence usually includes:

- contract or order;

- invoice or bill;

- proof of delivery or performance;

- payment reminders;

- demand for payment;

- debtor’s response, if any;

- interest calculation;

- proof of court fee payment.

In commercial disputes, the claimant should present all claims and evidence in the statement of claim. Evidence submitted later may be disregarded unless the party shows that it could not have been invoked earlier or that the need to use it arose later.

Step 6: Calculate court fees and litigation cost exposure

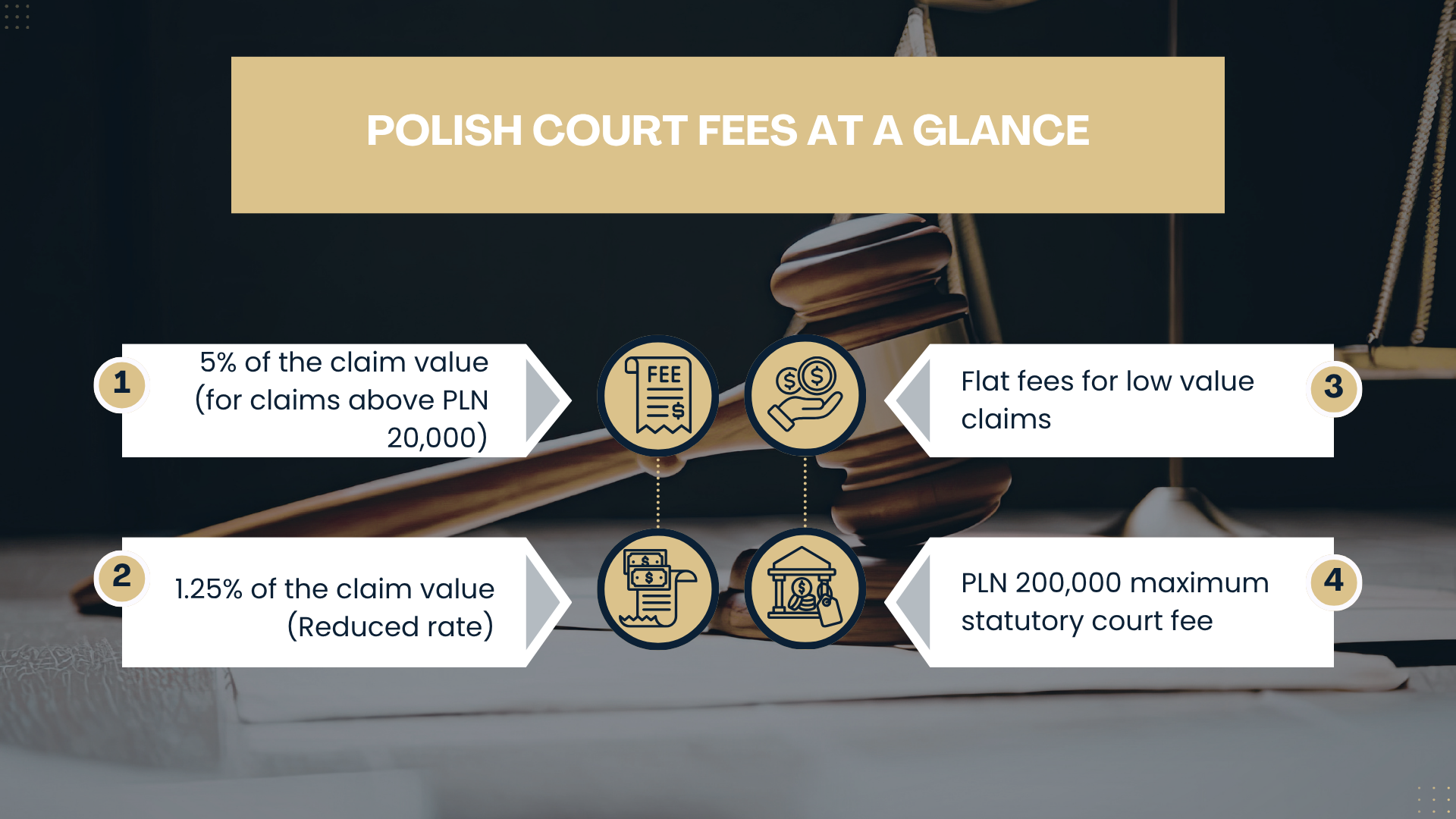

Court fees depend on the value of the dispute. If the value of the claim exceeds PLN 20,000, the filing fee is generally 5% of the claim value, with a maximum fee of PLN 200,000.

For smaller claims, flat fees apply depending on the value of the dispute. In commercial cases where the debtor acknowledged the debt, the claimant may benefit from a reduced fee of 1.25% of the claim value.

The court fee must be paid before the case starts. If the creditor wins, the fee may be recoverable from the losing party, but recovery still depends on the debtor’s solvency.

Step 7: Consider interim security

A creditor may apply for security before filing the lawsuit or during the proceedings. To obtain it, the creditor must make the claim plausible and show a legal interest in securing the claim.

Security may be useful where there is a risk that the debtor will dispose of assets before judgment. It can also create early pressure and improve the creditor’s enforcement prospects.

Security proceedings may take place without the debtor’s participation. As a result, the debtor may learn about the security only after the court has issued the relevant order.

Step 8: Enforcement by a Polish bailiff

After obtaining a final judgment, the creditor must obtain an enforcement clause. This creates an enforceable title that can be submitted to a public bailiff.

The enforcement application should indicate which debtor assets should be targeted. Enforcement may cover bank accounts, movable assets, remuneration, pensions, tax overpayments, property rights, claims against third parties, real estate or other property.

If the creditor does not know what assets the debtor has, the bailiff may be instructed to search for them. After receiving an advance for costs, the bailiff may take steps to identify the debtor’s assets.

Step 9: Enforcing a Polish judgment abroad

If the debtor has assets in another EU Member State, Polish judgments may be enforced under the Brussels I bis Regulation. This provides for automatic enforceability of judgments issued in another Member State without prior confirmation in separate proceedings.

Outside the EU, recognition and enforcement depend on applicable international agreements or local law. If no agreement applies, exequatur proceedings may be required in the foreign jurisdiction.

For cross-border creditors, this should be checked early. If the debtor’s main assets are outside Poland, enforcement strategy may be as important as the Polish court case itself.

Practical takeaway

Debt recovery in Poland should be treated as a staged process, not a single court filing. The creditor should first verify the debtor, then send a proper demand, test settlement options, secure the claim where possible and proceed to court only with a complete evidence package.

The most common practical risks are weak debtor verification, lack of proof that the demand was delivered, unsecured settlement and late submission of evidence in commercial disputes. Addressing these issues early may significantly improve the chance of actual recovery.

Foreign creditors planning or already conducting business in Poland can find more practical legal guidance in our legal guides. For assistance with debt recovery in Poland, contact Dudkowiak & Putyra at info@dudkowiak.com.